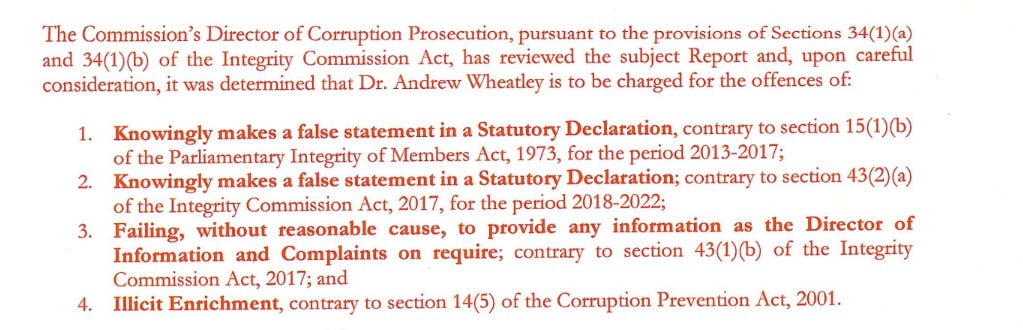

Jamaican Cabinet Minister Dr. Andrew Wheatley To Be Charged For Illicit Enrichment, Integrity Commission Rules.

Wheatley Rejects Commission's Key Finding Calling It "Patently False" and "Inaccurate."

Jamaica’s Integrity Commission has ruled that Dr. Andrew Wheatley, Minister Without Portfolio in the Office of the Prime Minister with responsibility for science, technology, and special projects is to be charged for illicit enrichment.

The Commission’s Director of Corruption Prosecution also ruled that he be charged with knowingly making a false statement, and failing, without reasonable cause, to provide information as required, according to documents tabled in the parliament on Wednesday.

The investigation concerned Wheatley’s statutory declarations submitted to the Commission for the years 2010 to 2022, mostly while he was Member of Parliament for St. Catherine South Central under the governing Jamaica Labour Party. The relevant period for the illicit enrichment calculations, however, was between 2013 and 2022.

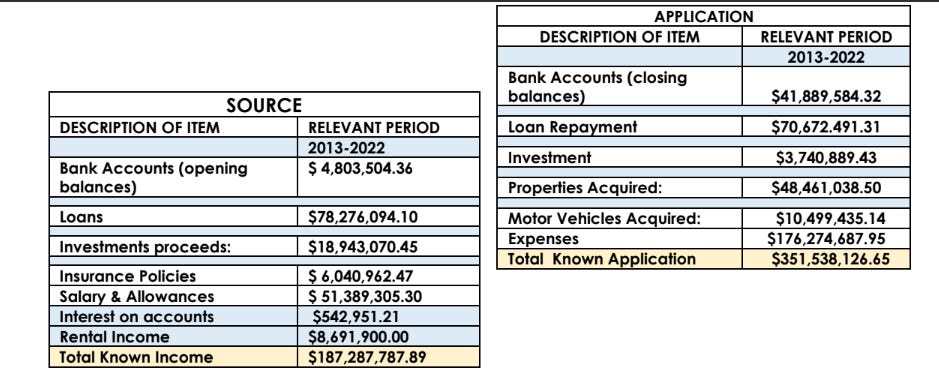

The Commission found that Wheatley was in possession of assets disproportionate to his lawful earnings to the tune of $164 million.

This was based on a calculation putting Wheatley’s total income at approximately $187 million, while his application—which includes closing balances in bank and investment accounts, loan repayments, investments, property and motor vehicle acquisitions and expenses — amounted to around $351 million ($187 million - $351 million = -$164 million).

According to the investigation report, Wheatley failed to provide an explanation which satisfies section 14(5) of the Corruption Prevention Act as to how he came by said assets. The investigation also revealed that Wheatley held assets which he failed to include in his statutory declarations in 2013, 2014, 2015 and 2021.

The Commission said the “foregoing omissions prima facie constitute offences under section 43(2)(a) of the ICA (Integrity Commission Act) and section 15(1)(b) of the Parliament (Integrity of Members) Act.”

Transactions Questioned by the Commission

There were extensive assets, liabilities, gifts and income that Wheatley declared in his statutory declarations but failed to provide additional information on when this was requested by the Director of Information and Complaints. The Commission said, it would appear he also failed to disclose an investment in a company, the particulars relating to the subdivision into lots and development and divestment of a plot of land that he jointly owned, and some commercial loans.

Among the gifts the Commission had questions about were six apartments.

The six apartments appear to have been part of a development on land acquired at East Kirkland Heights (Stirling Castle) by Wheatley and one Patrick Phipps in October 2011 with no registered mortgage.

In 2013, the property was sub-divided and developed into 20 strata lots, 14 of which were sold between 2014 and 2018, which wasn’t reflected in Wheatley’s statutory declarations for the period 2013 to 2018. In 2018, however, the report states, Wheatley began declaring rental income from six apartments in Sterling Castle, St. Andrew, which Wheatley had reported were acquired by way of “gift,” which he was asked to explain.

Wheatley responded to the Commission that sometime in 2010, Phipps, a building contractor who he’s known over the years, invited him to form a joint venture partnership to carry out housing developments. His role and function were to provide management of the JV, negotiate loans, identify development properties for acquisition, ensure timely approvals and sales, and, where possible contribute cash, which he did once by taking out a loan that was subsequently repaid by the JV.

Phipps’ role, meanwhile, was to negotiate builders’ credits, bank financing and provide cash equity where required by the financial institution.

Wheatley explained that his compensation was to be in the form of units in the completed development. This project happened to be one of the first projects undertaken. He explained that the six units represented his share of the profits and added that, since the titles were registered in both our names and only required removal of Phipps’ name, the transaction was annotated on the titles by the lawyers as “transfer by way of gift.”

Wheatley also indicated that the acquisition of the land was funded solely by Phipps, which Phipps confirmed. This caused the Commission to summarize that, “In essence, Dr. Wheatley, having not contributed any capital to the joint venture received six (6) units as compensation therefrom.”

Among Wheatley’s other properties acquired were two properties in Florida in the United States; a property in Drax Hall in St. Ann; lands in St. Elizabeth; and a piece of land in Stilwell. He also had investments in several companies including Techem Supplies; Price Tech Limited; Prosperity Realtor Company Limited; and Western Medical Centre.

Wheatley claimed to have purchased the Drax Hall property partly with earnings from Western Medical of which he was the sole proprietor. The business was subsequently closed in 2013, but not before receiving income of $45 million from the company between 2010 and 2013, $13 million of which, he said, was received in 2013 from the proceeds of the sale of the business.

Wheatley provided financial statements showing the company had earned revenue ranging from around $15 million to $26.7 between 2010 and 2013 with salary and wages ranging from $12.9 million to $17 million. An examination of its tax filings by the Commission, however, showed that in some years during the relevant period, the company filed nil tax returns, which is usually interpreted to mean that the business entity had not declared any income or expenses on the form even though Western Medical was reported by Wheatley to have had earnings.

For this, the DI referred the investigation report to the Tax Administration of Jamaica for an assessment to be made, and where necessary, for penalties to be imposed.

Wheatley Slaps Back

In a statement released to the media, through his attorney, Wheatley rejected as “patently false, inaccurate and grossly misleading” the Commission's finding regarding the $164 million disproportionality concerning his assets compared to his lawful earnings.

Wheatley called it “odd, unreasonable and unfair that in arriving at his conclusion, the Director of Investigations clearly decided not to take into account approximately 168-million in rental income which I lawfully accumulated and declared over the nine years.”

Wheatley continued that the Director of Investigation also failed to take into consideration “the lawful and verifiable payment sources utilized in respect of the repayment of approximately $50 million in loans obtained from financial institutions in the pursuit of my real estate business.”

As far as the six apartments which were declared to the Commission as gifts, Wheatley stated, “I entered into a joint venture which involved the purchase of land for development purposes. The initial arrangement with my business partner was to split ownership of the development along the lines of a 50/50 ratio. I was unable to meet my obligations and consequently the arrangement was adjusted to a 70 to 30 allocation. I managed the construction and negotiated credit. My 30 percent share of the development would amount to the proceeds of sale of six units. Instead of taking value in cash, I chose to have properties transferred to me. The Attorneys-at-Law handling the Joint Venture prepared the transfer indicating it was by way of a gift. The Director of Investigations is apparently not aware that, in the real estate industry, such a transaction is not an unusual commercial arrangement which developers may lawfully enter into.”

On the recommendation that he be charged for illicit enrichment along with the other charges, he said it will be “vigorously contested.”

Wheatley, who says he’s been cooperating with the investigation, attested, “I have lawfully acquired every dollar and every asset that I own. I intend to defend my reputation via the Court and am confident of a positive outcome.”

“There is no credible evidence to support the allegation that I acquired my earning by unlawful means and,” Wheatley said. “Should additional proof of this was required by the Director of Investigation, all he had to do is ask.”

How much did Wheatley pay in incone tax, in total and by year between 2011 and 2022?

Good article